-

January 2025 MyPlanIQ Portfolio Update

In this issue:

- 2024 Review

- Fund Analysis: Be Cautious with Options-Based Income Funds

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Expect a Bumpy Ride: Outlook for Stocks and Bonds in 2025

-

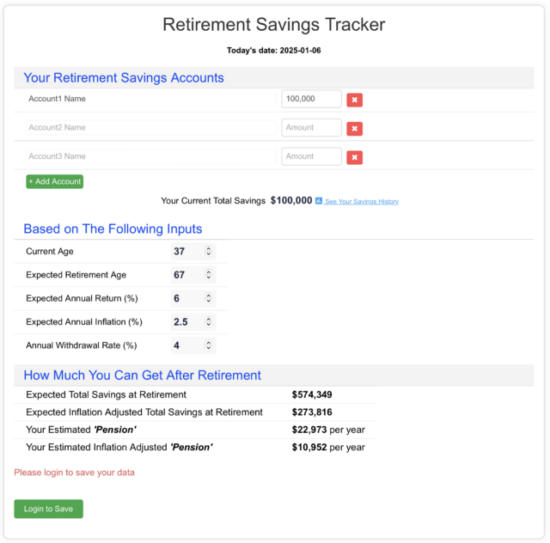

Retirement Savings Tracker and Future ‘Pension’ Estimator

In this issue:

- Gen X’s Retirement Savings Shortfall

- Introducing Retirement Savings Tracker & Future ‘Pension’ Estimator

- Retirement Savings Tracker

- Most Popular Bond Funds in 401(k) Plans

- Market Overview

-

Certificates of Deposit (CDs) vs. Treasuries: The Key Pros and Cons Explained

In this article, we summarize the pros and cons between CDs and Treasuries for fixed-income investors. Key Differences Between Certificates of Deposit (CDs) and Treasuries Factor CDs Treasuries Security – FDIC-insured up to $250,000 per depositor per bank. + Backed by the full faith and credit of the U.S. government, Treasuries are considered among the safest investments, with security that surpasses even FDIC insurance. – Limited insurance coverage for amounts above $250,000 at each bank. + No limit to the amount of protection. Yield + Generally higher yields for maturities of 1 year or longer. – Typically lower yields for maturities over 1 year. – Lower yields for shorter maturities compared to Treasuries. + Higher yields for short-term maturities (less than 1 year). Note: this could possibly change so double check yields before purchase. Taxes – Subject to both federal and state income taxes. + Exempt from state income taxes. – State tax impact can reduce effective yield, especially in high-tax states. + More tax-efficient, especially in high-tax states. Maturities – Limited availability for maturities beyond 5 years. + Wide range of maturities (4 weeks to 30 years). – Flexibility can be restricted depending on the bank’s capital needs and availability of brokered CDs in a brokerage like Schwab or Fidelity. + Extensive maturity options between 2023–2053. Liquidity – Less liquid, may involve fees or uncertainty of receiving original principal if sold early. + More liquid, with an active secondary market for easy resale. – Brokered CDs can be sold in secondary markets but may involve a fee. + Easier to sell with tighter bid/ask spreads. Strategy Considerations – Fewer maturity options for building a maturity CD ladder. + Easier to build a flexible bond ladder portfolio. Convenience + Banks often promote CDs with lower yields. – Has to rely on Brokerage to purchase/sell Treasuries most times Detailed Tax Impact Comparison: State Tax Impact CDs Treasuries For High-Tax States – State income taxes can reduce yield significantly (e.g., California, New York). + State income tax exemption offers a clear tax benefit. Example – In California, a 3-year CD yielding 3.90% after state taxes drops to 3.38%. + A 3-year Treasury yielding 3.51% remains unaffected by state taxes. Breakeven Tax Rate – For a CD to equal a Treasury’s yield, a state tax rate of ~10% or more may be required. + More tax-efficient for investors in high-tax states. Conclusion In summary:

-

Top 9 Most Popular Stock Funds in 401(k) Retirement Plans

Top 9 Most Popular Stock Funds in 401(k) Retirement Plans include actively managed funds by excellent managers and several ultra-low cost Vanguard stock index funds. It also features their latest return figures.

-

Top 11 Most Popular Bond Funds in 401(k) Retirement Plans

Top 11 Most Popular Bond Funds in 401(k) Retirement Plans include actively managed funds by award winning managers and ultra-low cost bond index funds. It also has its latest return figures.

-

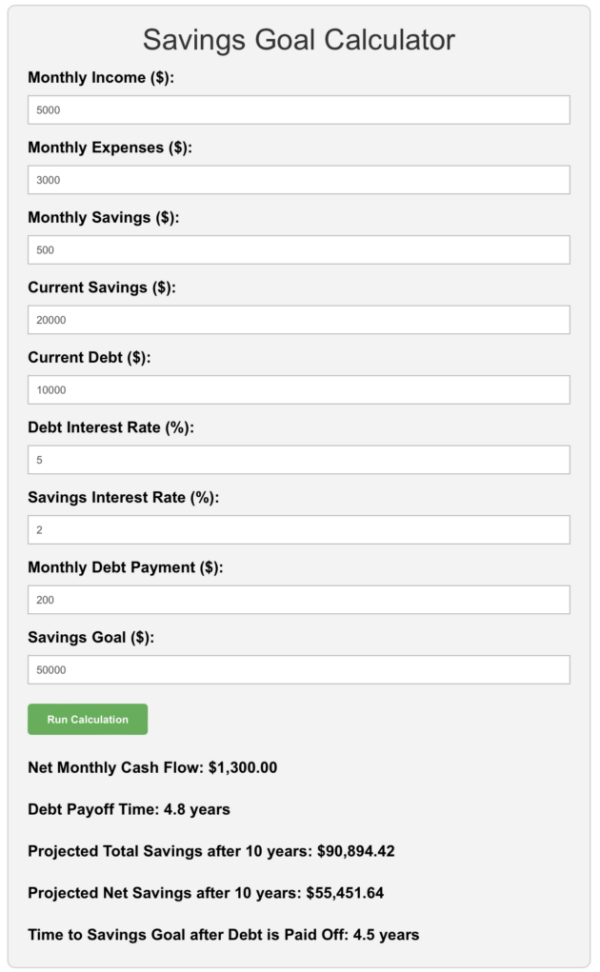

Smart Rules of Thumb to Manage Your Personal Debts

In this issue:

- Student Loan Payoff and 401(k) Match

- Smart Rules of Thumb to Manage Your Personal Debts

- Savings Goal Calculator: Payoff Debt and Save More

- Most Popular Bond Funds in 401(k) Plans

- Market Overview

-

Health Insurance Costs Far Outpace Inflation: How to Protect Your Retirement Savings

In this issue:

- Medicare Cost Increases for 2025 & Ever Rising Health Insurance Cost

- How to Safeguard Your Retirement Savings from Increasing Health Care Costs

- Investment Return Calculators for Funds, Portfolios or Stocks

- Most Popular Stock Funds in 401(k) Plans

- Market Overview

-

December 2024 MyPlanIQ Portfolio Update

In this issue:

- Tactical Asset Allocation Portfolios In-Depth Update

- Fund analysis: U.S. stock momentum factor ETFs

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

-

The Four Essential Steps for 401(k) Investments

In this issue:

- Leaving your company: things to consider for your company 401(k) account

- The Four Essential Steps for 401(k) Investments

- How to Determine the Amount to Contribute to Maximize Your Company Match

- Thrift Savings Plan: The Largest Public Sector Workers’ Retirement Savings Plan

- Market overview: Enjoy the season but don’t be complacent

-

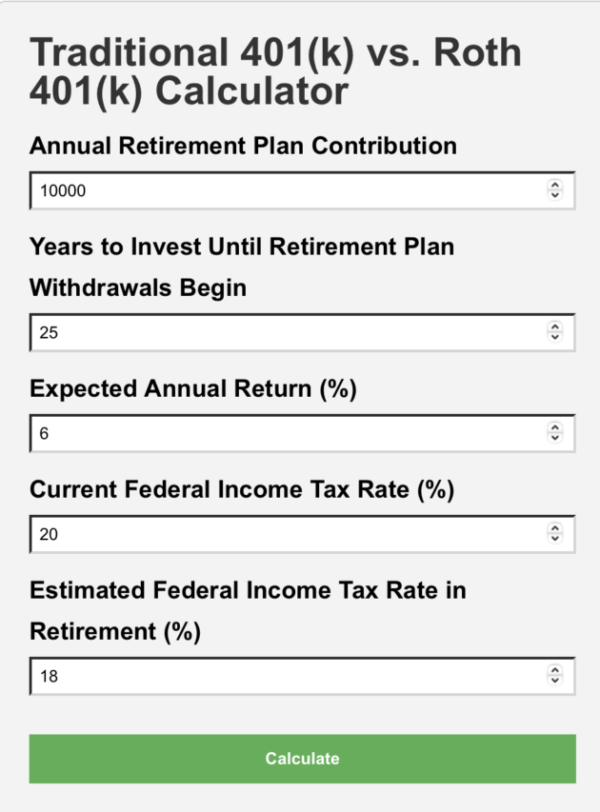

Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

In this issue:

- Retirees’ credit card debt increased!

- Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

- Traditional 401(k) vs. Roth 401(k) Calculator

- Top 15 employers with the highest employer match rate per employee

- Market overview: Year-end stock rally?

-

IRA and Roth IRA Contribution Limits: Annual Caps, Income Restrictions, and 401(k) Considerations

When planning your retirement savings, understanding the annual contribution limits for Individual Retirement Accounts (IRAs), Roth IRAs, and how these interact with 401(k) contributions is essential. Below is an itemized breakdown of contribution limits, income caps, and key considerations. 1. Traditional IRA Contribution Limits (2024) 2. Roth IRA Contribution Limits (2024) 3. Non-Deductible Traditional IRA Contributions 4. Considerations When You Also Contribute to a 401(k) 5. Caution: Pro-Rata Rule for Roth IRA Conversions If you plan to make non-deductible IRA contributions and later convert them to a Roth IRA (commonly known as a “backdoor Roth IRA”), be aware of the pro-rata rule. This rule requires you to calculate taxes on the conversion based on the proportion of pre-tax and after-tax funds across all your traditional IRAs. By balancing 401(k) and IRA contributions, you can maximize tax benefits and long-term retirement growth. If income caps restrict your IRA options, consider strategies like non-deductible IRA contributions or a Roth IRA conversion. In terms of non-deductible IRA contributions, you’ll need to track its basis for tax purposes.

-

YieldMax ETFs Returns & Comparison

This page tracks YieldMax ETFs Total Returns (Price Appreciation and Dividend Reinvested). It also compares each ETF with its underlying stock.

-

A 6% Default Retirement Savings Rate Is Becoming the Standard—But Is It Enough?

In this issue:

- A 6% default retirement savings rate Is becoming the standard—but Is It enough?

- Bonds for the long-term: why a 60% stock/40% bond portfolio?

- Retirement calculator: why a 12% to 15% savings rate

- Top 15 employers with the highest employer match per employee

- Market overview: renewed inflation threats

-

How to Maximize Tax-Deferred Retirement Savings Beyond the $69,000 ($70,000 for 2025) IRS Limit

For individuals with multiple income streams, such as physicians, small business owners, startup founders, entrepreneurs, and consultants in tech or other fields, it’s possible to exceed the IRS’s annual limit for tax-deferred retirement savings ($69,000 for 2024 and $70,000 for 2025).

-

Stocks for The Long Term: Why They Outperform Bonds

In this issue:

- Retirement savings: what Morningstar retirement model reveals

- Stocks for the long-term: why they outperform bonds

- Investment arithmetic: investment calculator

- The billion-dollar employer contribution club

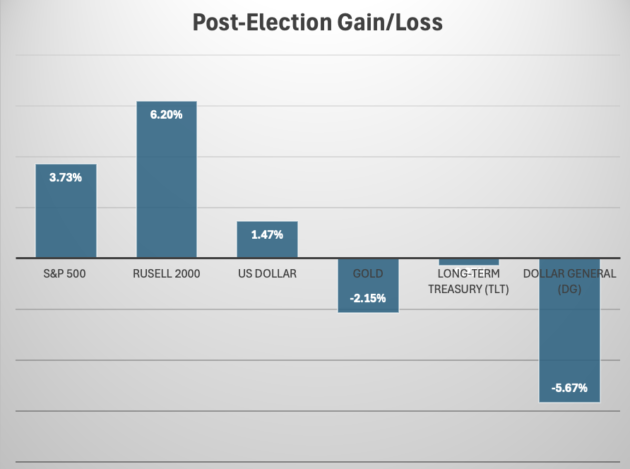

- Market overview: post-election stock rally, inflation …

-

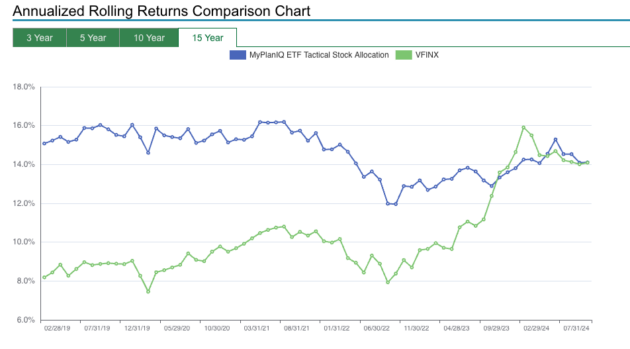

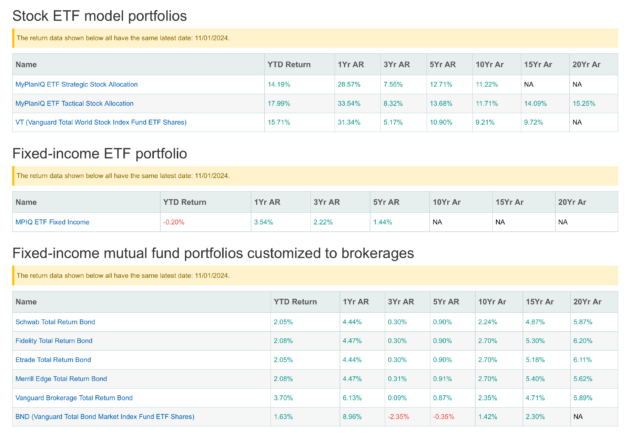

MyPlanIQ Monthly Portfolio Update

We explain our premium portfolios and discuss their holdings. We further discuss several funds that are related to our portfolios. Current economic and financial conditions are also discussed.

-

When to Retire Matters—A Lot!

Retiring at the peak of a bull market or right after a bear market can significantly impact your retirement finances.

-

How to Become a 401(k) Millionaire?

Save & invest consistently, dollar-cost average your way to be a 401k millionaire.

-

Introducing the Save More, Grow Wise Newsletter

Introducing Save More, Invest Wise Newsletter that focuses on retirement savings, retirement investments, etirement planning, personal finance topics such as debts and spending, and tools.

-

Comparing Yields on Various Types of Personal Loans: Should You Pay Off or Invest?

Comparing Yields on Various Types of Personal Loans: Should You Pay Off or Invest? Loans are a big part of managing your money, and it’s important to get a handle on how their interest rates work so you can make smart choices. Whether you’re buying a house, getting a car, paying for school, or just covering your expenses, it’s all about knowing when it’s okay to borrow, when to focus on paying things off, and what to do with any extra cash. Don’t forget—sometimes safe investments like Treasury bonds or short-term bond funds might be a better option for your money than paying down certain types of debt if those debts’ interest rates are lower than what’s paid by these safe bond investments! Let’s explore the common types of personal loans—mortgages, credit card debt, car loans, student loans, and other personal loans—and discuss when paying off loans makes sense compared to safe investment options. Loan Types and Their Yields 1. Mortgage Loans

- Yield Range: 2-7% annually

- Purpose: Used to finance the purchase of a home.

- Features:

- Mortgages tend to have the lowest interest rates among personal loans, especially with a fixed-rate, 30-year term.

- Interest may be tax-deductible.

- Consideration: With low interest rates, paying off a mortgage early often isn’t necessary, particularly if you can earn more by investing elsewhere. However, the funds you have allocated to pay off the mortgage should not be touched for other purposes, as it ensures your ability to meet future obligations.

2. Credit Card Debt

- Yield Range: 15-25% annually

- Purpose: Typically used for everyday expenses, emergencies, or convenience.

- Features:

- Credit card debt has one of the highest interest rates, quickly accumulating if not paid off monthly.

- Consideration: This is the type of debt you should pay off as quickly as possible. The interest rates are far too high to justify holding onto the debt while investing elsewhere.

3. Car Loans

- Yield Range: 4-10% annually

- Purpose: Used to finance the purchase of a vehicle.

- Features:

- These loans usually come with fixed rates over a term of 3-7 years.

- Cars depreciate quickly, which makes financing them costly in the long run.

- Consideration: Depending on the interest rate, paying off a car loan early could save you on interest, but it may not be the best move if your loan rate is low.

4. Student Loans

- Yield Range: 4-8% annually

- Purpose: Helps finance higher education.

- Features:

- These loans often come with favorable repayment terms, including deferment and income-based repayment options.

- Consideration: Paying off student loans isn’t urgent if your interest rates are low, especially when other higher-interest debts or better investment opportunities are available.

5. 401(k) Loans

- Yield Range: Prime rate + 1% to 2% (e.g., if the prime rate is 7.5%, the loan’s interest rate will be 8.5% to 9.5%).

- Purpose: Allows borrowing against your retirement savings for emergencies or significant expenses.

- Features:

- Repayments consist of principal and interest, typically made monthly or bi-weekly via payroll deductions.

- Interest repaid goes back into your 401(k), effectively “paying yourself.”

- No credit checks or third-party lender involvement.

- Consideration:

- Reduces the growth potential of your retirement savings during the loan period.

- Leaving your job could require repaying the balance as a lump sum, typically within 60 to 90 days. Failure to do so may result in taxes and penalties.

- Best used as a last resort to avoid jeopardizing long-term retirement goals.

6. Other Personal Loans

- Yield Range: 6-15% annually

- Purpose: Used for a variety of personal expenses, such as medical bills or debt consolidation.

- Features:

- These loans tend to have higher interest rates than secured loans like mortgages but lower than credit card debt.

- Consideration: Paying off high-interest personal loans can be financially wise, but if your rate is closer to the lower end, safe investments may outperform.

Example 1: Should You Pay Off or Invest? Let’s say you have $50,000 in cash and are trying to decide whether to pay off your mortgage with a 4% interest rate or invest in a low-risk option like U.S. Treasury bonds yielding 4.5%.

- Paying Off the Mortgage: If you pay off your mortgage, you effectively “earn” a 4% guaranteed return, which is the interest you won’t have to pay.

- Investing in Treasuries: By investing in Treasury bonds at 4.5%, you’d earn a slightly higher return—$2,250 annually compared to the $2,000 saved by paying off the mortgage.

Conclusion: In this scenario, investing in U.S. Treasuries offers a marginally higher return with the same level of safety. However, the decision may hinge on factors like personal comfort with debt and liquidity needs. If being debt-free provides peace of mind, the difference might not be worth it. Example 2: Why You Shouldn’t Pay Off a 2.2% Mortgage Early Now let’s say you’ve got a 30-year fixed mortgage at 2.2%, one of the lowest rates seen in recent years. Should you use extra cash to pay it off early?

- Paying Off a 2.2% Mortgage: Paying off the mortgage would save you 2.2% annually in interest payments—a low return considering the alternatives.

- Investing in Ultra-Safe Bonds: With U.S. Treasury bonds or ultra-short-term bond funds currently yielding 4-5%, you could almost double your return by investing the cash instead of paying off your mortgage. These investments are also very low-risk, making them an attractive alternative.

Conclusion: In this case, it doesn’t make much sense to pay off a mortgage with such a low interest rate. By investing in safe options like Treasury bonds, you can achieve a higher return with minimal risk. However, it’s crucial that you don’t use the funds intended to pay off the mortgage for anything other than investing. The funds should remain liquid and accessible in case you need them for your mortgage payments down the road. Rules of Thumb to Manage Personal Loans

-

Pay Off High-Interest Loans First

- Example: It’s a no-brainer to first manage your credit card debt that obviously has the highest interest rate! If you have a credit card debt with a 20% APR and a car loan with a 6% interest rate, prioritize paying off the credit card to save on interest costs.

-

Consider Loan Advantages

- Example: A 401(k) loan allows you to repay yourself with interest, which can be more advantageous than taking out a personal loan with higher interest rates. Similarly, some mortgages or student loans offer tax benefits worth retaining.

-

Refinance to Lower Interest Rates

- Example 1: Switch your credit card debt to another credit card debt that has lower interest rate or borrow from your 401(k) to pay off the highest interest rate credit card debt if necessary!

- Example 2: If you’re repaying a 10% personal loan, consider consolidating it into a 6% home equity loan to lower your interest expenses.

Other Key Considerations

- Current Loan Interest vs. Investment Return: If your loan’s interest rate is significantly lower than what you can earn with a safe investment, investing the cash is usually the smarter move.

- High-Interest Debt: Always pay off high-interest debt first (e.g., credit card debt). The interest rates are far higher than what you could safely earn through investments.

- Emergency Fund: Always maintain an emergency fund before paying off debt or investing. This ensures that you have liquidity for unexpected expenses.

- Mortgage Payoff Strategy: While paying off a mortgage can be a guaranteed return, low-rate mortgages (like the 2.2% example) shouldn’t be paid off early if you have access to higher-yielding, low-risk investments. But remember, the funds should remain liquid and be used only for their intended purpose.

- Personal Peace of Mind: If being debt-free offers you significant emotional relief, it may outweigh the financial benefits of investing, even if the math favors the latter.

By carefully balancing loan interest rates with safe investment opportunities, you can maximize your financial outcomes while maintaining security. Safe investments like U.S. Treasury bonds or ultra-short-term bond funds often provide better returns than low-interest loans, but high-interest debt should always be addressed first.